The old axiom that “the only thing that’s constant is change” applies to the paper industry. We continue to find ourselves dealing with a market full of uncertainty and change.

US graphic paper markets have been more stable in the first quarter of 2023, although we see a lot of familiar indications that traditionally point toward more price changes: falling operating rates, weakening demand, growing import pressure, and high printer inventories.

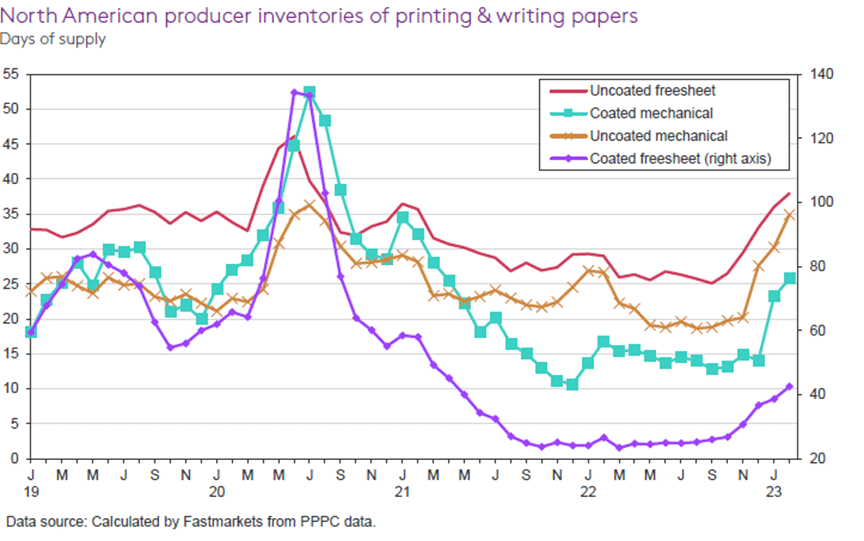

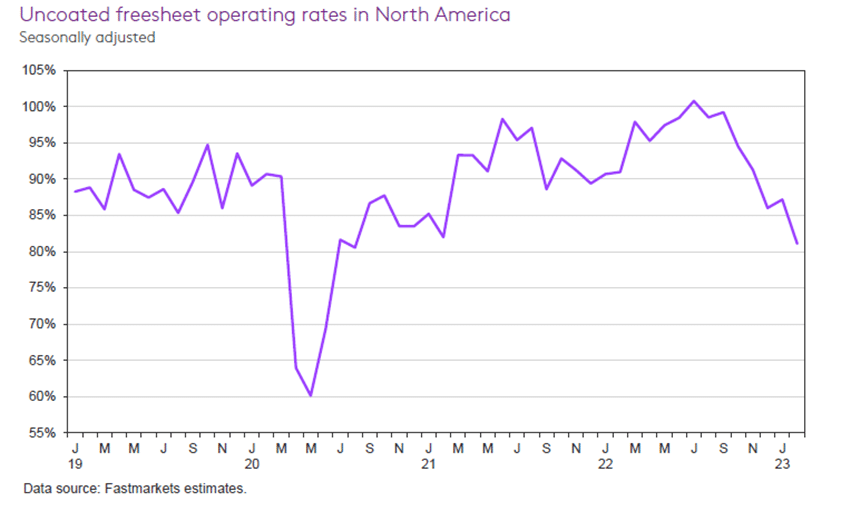

We saw an inventory buildup at both mills and printers in the back half of 2022, driven by increased imports and printers purchasing all their allocated paper tonnages. While all uncoated mills are off allocations, there are still “soft allocations” in the coated market. 2022 was the largest import year in our industry since 2015. As inventories rose, the industry also experienced a roughly 20% drop in print operating rates from Q4 2022 to now. This equates to 1.7 million tons of excess paper capacity. In our Q4 2022 paper market update we predicted Q1 2023 would have printers working down their current inventories. Inventory is being decreased by printers, but there is still a lot more to be consumed, and we expect the industry will take until Q3 before those inventories are closer to normal levels. For the health of the paper and print industry, prices need to stay around current levels until excess inventories are consumed.

We expect stable paper pricing in Q2

With increased paper prices over the past two years, paper mills have been able to operate with healthy profits, something that recent history did not allow. Mills are now able to make longer-term decisions and keep away from immediate supply chain reactions to change the supply chain balance. Being on better financial footing allows mills to take scheduled downtime for maintenance and even shut down a mill line temporarily. These maneuvers are also levers they use to balance inventories in ways that enable them to maintain existing price levels.

The risk is that these maneuvers don’t line up with forecasted demand build-up in the summer months, which may result in another possible paper shortage. Ultimately time will tell if the industry overcorrected. If the market rebounds, there could be a challenge of capacity in Q3/Q4 as mills are not building inventory.

Mill Updates

In February, Pactiv-Evergreen had idled one machine at the Canton, North Carolina mill. In March, they announced the entire mill will close in Q2 2023, removing 240,000 tons of uncoated freesheet capacity.

ND Paper’s Biron mill has left coated mechanical production to convert to recycled containerboard.

Pixelle announced it would be closing its Jay, ME mill before April, which is earlier than expected. The mill produces specialty label and release papers, as well as industrial and packaging solutions for e-commerce and food service. One of their main challenges was recovering from an explosion of one of the mill’s pulp digesters in 2020. Pixelle has also closed the Androscoggin mill’s specialty production.

Billerud announced plans to relaunch its OptiLabel HB made at the Quinnesec mill. This specialty paper is designed for high-end pressure-sensitive label applications. The company already makes OptiLabel HB and UniSil release liners at the Escanaba mill.

The Finnish port strike came to an end in late February. This strike lasted two weeks and had a dramatic effect on Finland’s logistics sector, halting operations at many ports. Fastmarket’s World Pulp Monthly estimated that each week of the strike could result in the blocking of about 105,000 tons of market pulp, an estimated 10.3% of global shipments per week.

Uncoated Freesheet

North American uncoated freesheet inventories started at high levels in 2023. This is a result of the strong demand we saw in the second half of 2022 due to inventory building and warehousing activity, which resulted in strict 2022 allocations. We now have ample inventories in 2023 at the same time demand has weakened. Demand is expected to decrease by 6% in 2023, bringing the market back to 2020 levels. This prediction is driven by import pressures and capacity reductions that have already been announced, as mentioned earlier with Pactiv Evergreen’s closure of their Canton, North Carolina mill.

Operating rates, which averaged 95% in 2022 due to strong demand and printers using their allocations to build inventory levels, dipped to 84% in the first two months of 2023. Operating rates could be in the 91% range in the second half of 2023 due to the Canton closure.

Coated Papers

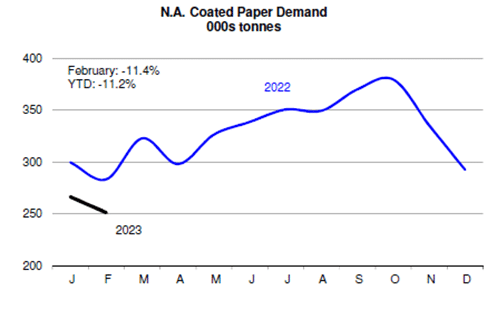

Coated freesheet operating rates took a steep dive to 64% in February. The low operating rates are from a combination of decreased demand and heavy import pressure.

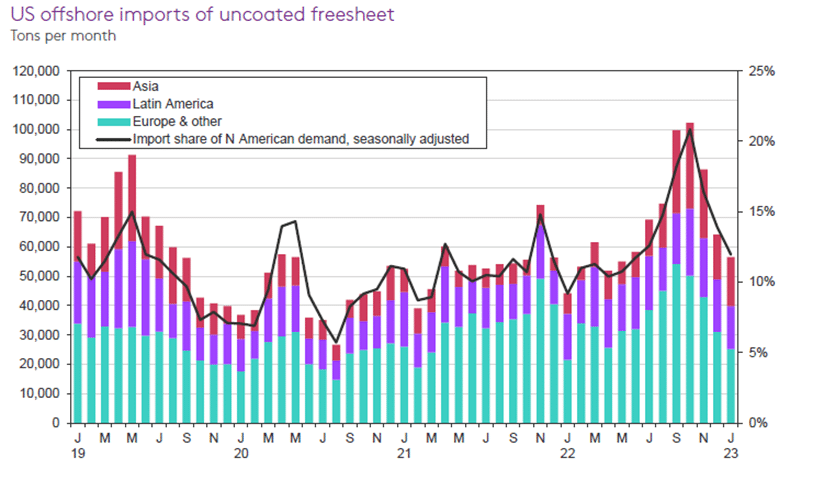

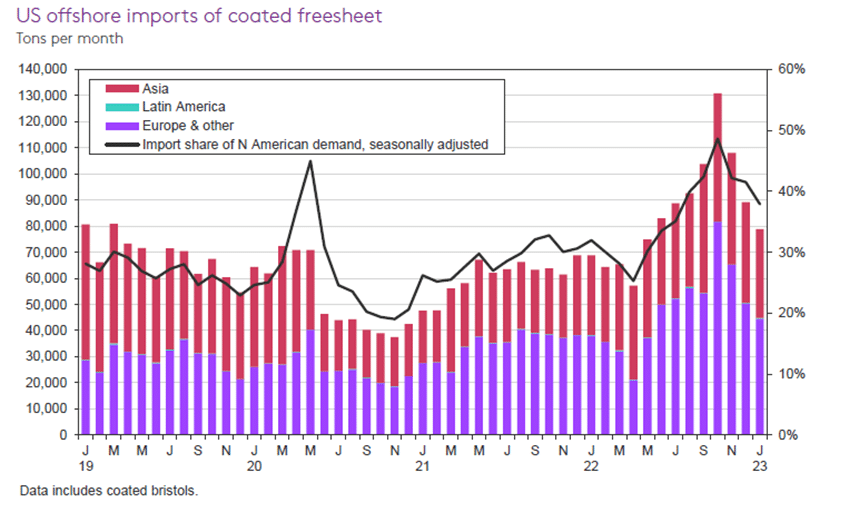

In December of last year, imports accounted for 42% of coated freesheet demand and 35% of coated mechanical demand. Imports continue rising year-over-year. In February, they were up by 37%.

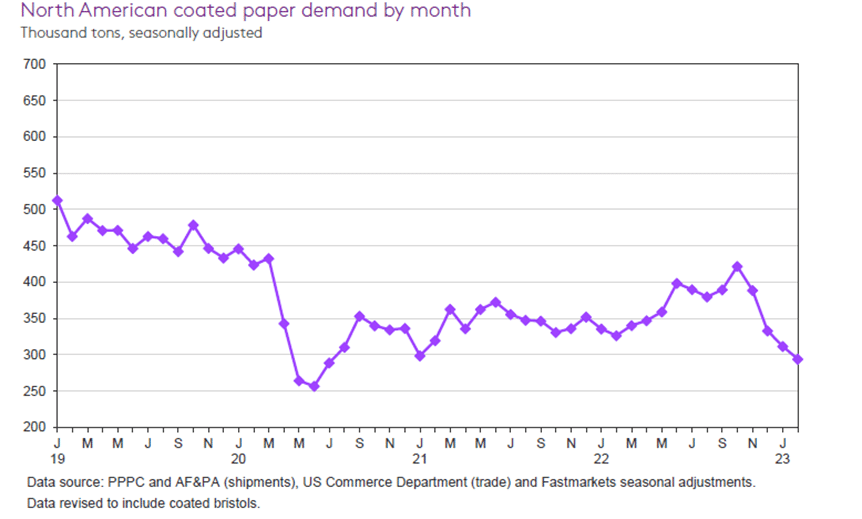

Coated paper demand appears to be down about 20% from Q4 2022, again reflecting a major inventory drawback in 2023. Coated mechanical demand was already expected to drop because of the Biron mill exit. Like other grades, prices continue to hold steady.

Closing Thoughts

SPC will continue to monitor market signals to help you plan your future print projects. Our biggest piece of advice remains the same: Plan well ahead when you can. We recommend allowing 90 days for large paper orders. There are often times when a 3 – 5 week lead time is achievable but it is not always possible and better never to be left to chance.

We expect the market to tighten towards the end of Q2 and the beginning of Q3. We believe we may find the market demand to be higher than the supply chain can handle in the back half of Q3 and into Q4 for the direct mail holiday rush.

Reach out to your SPC rep to plan ahead for success. Discuss securing your paper before mills consider going back on allocation.

Contact Ryan LeFebvre at ryanl@specialtyprintcomm.com for assistance in making your DM programs a success.