On May 28, SPC held an exclusive roundtable discussion featuring representatives from Midland, Sappi, and Domtar. The group provided critical insights on the current state of the paper market, empowering SPC clients to make well-informed business decisions.

Paper Market Expert Panel

- Craig Busby from Midland Paper

- Bryce Petty from Sappi

- Sam Ankony from Domtar

Key Discussion Points

- Paper prices have increased across the board due to inflation, rising cost of fuel and ongoing tariff uncertainty, with both coated and uncoated freesheet suppliers announcing multiple price increases.

- Industry consolidation and capacity reductions are reshaping the market.

- Lead times for uncoated freesheet orders are extending into September or later at some mills, while coated paper availability is also tightening due to production issues, downtime, and allocations at mills.

- Mills are keeping strong pricing discipline and lean inventories despite moderate demand, indicating a shift from the oversupplied market, though panic buying is not expected.

- Prices are expected to remain steady through the rest of 2026

- That is, as long as the world economy allows.

Market Conditions & Industry Health

- Our experts believe the market is heading into more stable conditions despite all the announced closures.

- The coated freesheet side is fairly healthy due to capacity reductions, but the costs are a huge concern.

- The rising costs of fuel and inflation are major factors behind the recent price increases. Additionally, tariffs on imported materials also contribute to this issue for the coated side.

- The panel confirmed these increases are cost-recovery and demand-driven.

- The busy political season is driving a lot of demand; direct mail advertising for elections is relatively high and is expected to increase.

- The major industry change that has permanently altered paper economics is mills right-sizing their capacity to demand.

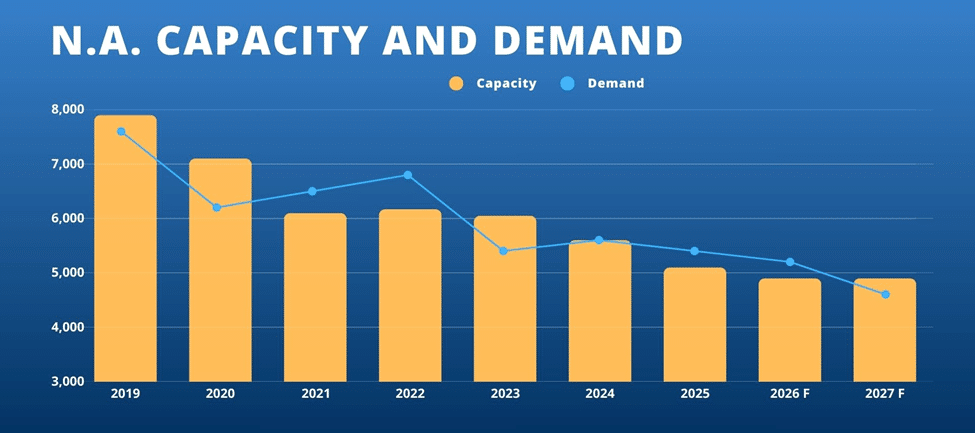

- Capacity reduction from the NA paper market

- Since 2021, the uncoated market has had 2.2 million tons of capacity removed.

- More than 300,000 tons have removed from the coated market.

- Our experts shared their opinions about the relatively healthy paper market and find themselves in decent positions with a good supply/demand balance. One indicator is the operating rates.

- Both Sappi and Domtar are operating in the low 90% range, which is ideal, meaning it is “comfortably full.”

- 85% and lower indicate a soft market.

- 95% is a very tight market where most people are on allocation.

Pricing, Cost Structure, & Mill Economics

- Reinvestments

- Sappi annually spends $100-$150 million on paper machines for maintenance and updates.

- Sappi is coming off a $500 million capital investment on the packaging side and converting a machine.

- Sappi annually spends $100-$150 million on paper machines for maintenance and updates.

- Paper prices softening

- In an ideal world, UFS would soften prices if the market saw a huge influx of imported paper.

- The expert panel predicted prices will be steady throughout the rest of the year.

- Sappi and UPM European have officially entered into a signed 50/50 joint venture, running as a separate organization.

- The European coated market is volatile and struggling.

- Sappi aims for this to achieve a positive outcome for the European market.

Capacity, Lead Times, & Product Availability

- Inventory levels

- Some mills have healthy supplies, while others have limited inventories.

- Manufacturers’ goals are to have a conservative amount of inventory.

- Domtar is committed to having inventory on the floor, especially for sheetfed and on the common roll sizes.

- Sappi has low inventory with the mindset of only making what the market and demand can take.

- Some mills have healthy supplies, while others have limited inventories.

- The market is seeing tightness for heavyweight coated (caliber grades).

- Cover will be tight, having only two machines in North America plus the impact of the upcoming election season.

- Boise is allocating uncoated freesheet.

- Lead times for the fall

- Our panel advised the audience to start communicating now what their expectations are for the rest of the year.

- Sappi is already blocking out tons into September.

- Uncoated mills are out to November.

- Domtar manufacturing dates are in the three-week time frame.

- Our panel advised the audience to start communicating now what their expectations are for the rest of the year.

- Expected downtimes

- Both Sappi and Domtar don’t have any scheduled downtime for the rest of 2026.

- Sylvamo announced an extended scheduled maintenance downtime at its Eastover, South Carolina mill.

- Tragedy struck at the NORPAC Longview Mill with a chemical tank implosion; therefore, paper machines are currently shut down.

Tariffs, Imports, & Global Supply

- Imports are down 15% in the coated freesheet market.

- Imports play a big role in CFS due to the capacity reductions and demand.For coated freesheet, the sheet side is 70% usage from imports and webs are about 20% usage.

- Uncoated freesheet historically is 12-15% on imported paper.

- Uncoated freesheet saw a recent spike in March, rising to 18% due to temporarily-lifted tariffs.

- Importance of imports

- Imports are important to the coated side to handle demand.

- Establishing a balance is essential to the stability of capacity.

- Imports are important to the coated side to handle demand.

- Tariff rates are generally settled into pricing structure.

Innovation & Looking Forward

- Our panel shared their thoughts about direct mail…

- Single most consistent and dependable driver of our markets.

- Direct mail drives demand and balances out paper machines.

- The market is relatively stable now, but anything can happen, as we have seen

- What the mills can control seems to be in good condition.

- Planning perspective

- The most important aspect is to communicate to SPC your projections so that we can inform merchants and mills to prepare and secure the necessary tonnage. While we don’t need exact numbers, an estimate will help in allocating paper.

- Develop a programmable relationship to forecast the frequency and size of printing for future projections. Any opportunity to forecast will be beneficial, especially given how unforeseen circumstances can arise.